What taxes do you have to pay when selling a house?

Fernando Orozco-Loza

Última actualización: 2026-05-04

Fernando Orozco-Loza

Última actualización: 2026-05-04

Understanding the taxes involved when selling a house is crucial for any homeowner. This process can be complex and varies based on several factors including profit, ownership duration, and local laws. It’s important to grasp these details to avoid unexpected costs.

If you are planning to sell or buy a property, schedule a free consultation with Fernando Orozco-L to guide you in adopting the best strategy and achieving the best results.

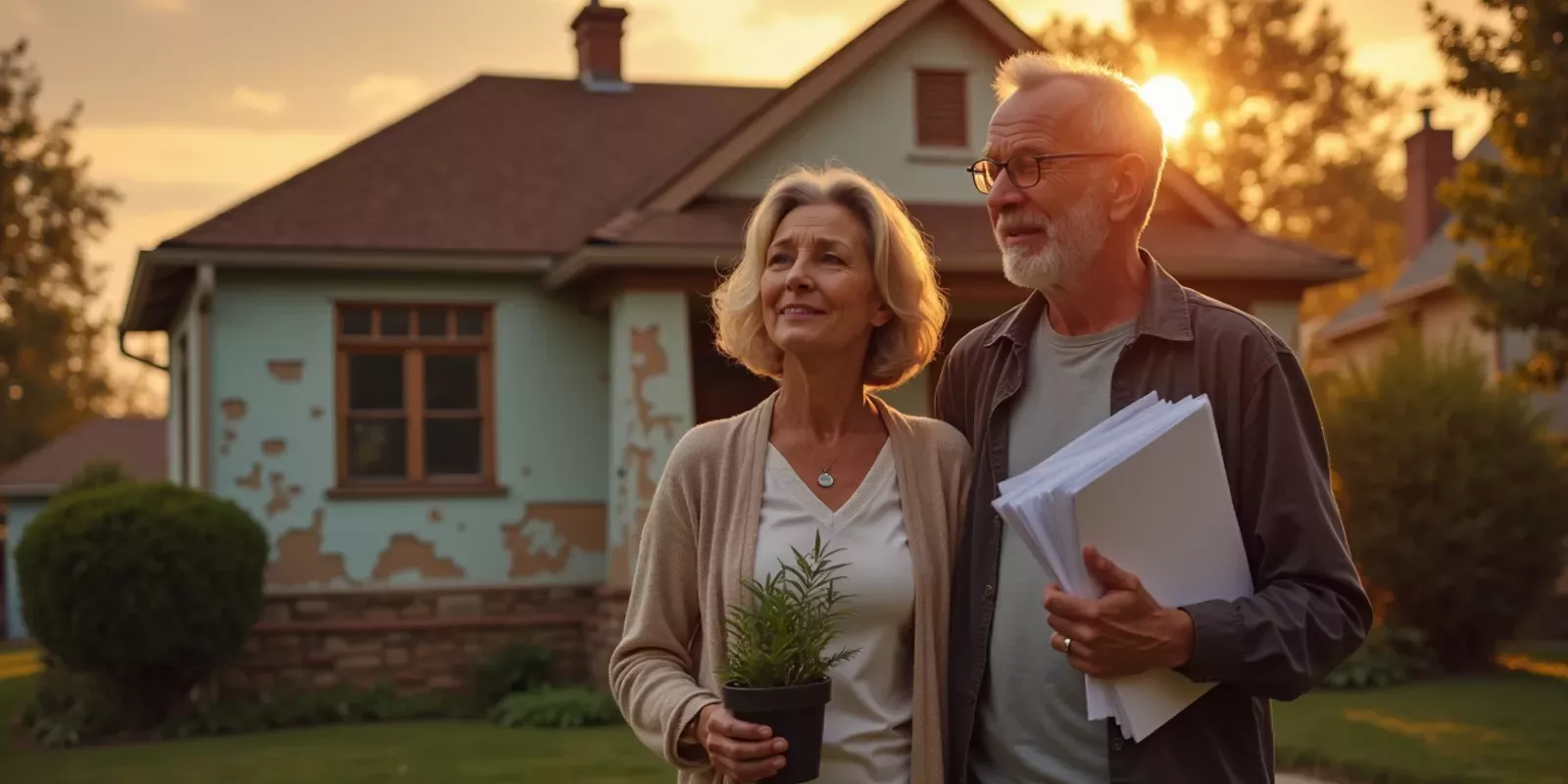

When I sold my first home, I was surprised by how many taxes applied. Most people think only about the selling price and moving costs. However, taxes can significantly affect your bottom line. Understanding which taxes you may owe is vital in making informed decisions about your sale.

There are several key taxes that sellers must consider, with capital gains tax being the most significant. In this article, I’ll break down what you need to know about each of these taxes, share real-life examples, and answer common questions to help you navigate this aspect of home selling.

Capital gains tax is typically the most substantial tax you will encounter when selling your house. This tax applies to the profit you make from the sale. If you sell your home for more than you paid for it, the profit is considered a capital gain.

The IRS allows certain exemptions on capital gains tax. For instance, if you’ve lived in your home for at least two out of the last five years, you may qualify for an exclusion of up to $250,000 if you're single or $500,000 if married filing jointly. These exemptions can significantly reduce your taxable gain.

To calculate your capital gain, subtract your adjusted basis in the property (the original purchase price plus any improvements made) from the sale price. For example, if you bought a house for $300,000 and sold it for $450,000 after making improvements worth $50,000, your capital gain would be:

$450,000 (sale price) - ($300,000 + $50,000) = $100,000 (capital gain)

In addition to federal capital gains tax, many states impose their own taxes on real estate sales. The rate can vary widely depending on where you live. Some states have no income tax but impose transfer taxes instead.

A transfer tax is charged when a property changes hands and is typically calculated as a percentage of the sale price. For example, if you're in a state with a 1% transfer tax and sell your house for $500,000, you'd owe $5,000 in transfer taxes.

Some municipalities may also impose additional local taxes on real estate transactions. Always check with local authorities or consult with a real estate professional to get accurate information regarding local taxation.

Consider Jane, who purchased her home for $200,000 twenty years ago. After several upgrades and a booming market, she sold it for $600,000. Because she lived in her home for over two years, she qualifies for the full exclusion on her capital gains tax. She doesn’t owe anything on her profit of $400,000.

Then there’s Mike who bought a fixer-upper for $250,000 and sold it just one year later for $350,000 after some renovations. Since he didn’t meet the two-year residency requirement, he must pay capital gains tax on his entire profit of $100,000.

Susan had to sell her house after moving out of state due to work. She purchased her home for $400,000 but sold it for $500,000 after three years. Although she lived there long enough to qualify for some exclusions, she will still owe taxes because her gain exceeds the allowable exemption limits.

If you're unsure about your situation regarding home sale taxes, I encourage you to reach out and discuss it!

Capital gains tax is a tax on the profit made from selling an asset like real estate. It applies when the sale price exceeds the purchase price.

Your basis includes what you paid for the property plus any improvements made over time minus any depreciation taken if applicable.

If you sell your home at a loss and it doesn’t qualify as an investment property or business asset, you generally cannot deduct that loss from your income taxes.

The primary exemption available is related to residency rather than being a first-time seller; however, first-time homebuyer programs may provide assistance with purchasing but not selling.

You can minimize your liability by holding onto the property longer to benefit from exclusions or by timing your sale carefully based on market conditions.

I’m here to help clarify any uncertainties regarding real estate transactions!

Navigating taxes when selling a house can be daunting. Each situation has unique factors that influence what you'll owe. With careful planning and understanding of local laws and regulations, you can effectively manage these obligations.

If you're looking for guidance tailored specifically to your needs or want assistance with navigating this process smoothly, don’t hesitate to reach out to me directly! I’m Fernando Orozco-Loza—your trusted expert in real estate matters—and I’m here to help.

El sector inmobiliario va más allá de comprar o vender una casa. Se trata de tomar decisiones importantes con confianza.

Cada cliente es diferente, por eso ofrezco un enfoque personalizado. Conozco el mercado de West Michigan y utilizo una comunicación clara y estrategias modernas para lograr resultados reales.

Mi prioridad es la transparencia, proteger sus intereses y hacer que el proceso sea simple y sin estrés. Conmigo, tendrá un asesor de confianza comprometido con su éxito.

Essential Habits of Successful Michigan Real Estate Investors

Successful real estate investors in Michigan share key habits like continuous learning, networking, goal-setting, financial discipline, embracing technology, and resilience. These practices empower you to navigate the market confidently and achieve your investment goals.

The Impact of War on Housing Prices

The impact of war on housing prices is significant and multifaceted. Conflicts can lead to property destruction, population displacement, and economic instability, resulting in fluctuating real estate markets. This article explores these effects through various case studies.

What Low-Cost Improvements increase my Home Value?

Discover low-cost ways to increase your home's value through strategic improvements. From budget-friendly kitchen remodels and landscaping enhancements to fresh paint and decor, small changes can yield significant returns, making your home more appealing and valuable.

![]()

![]()